Among the biggest success stories of the last 20 years has been the huge expansion of financial inclusion. To get from fewer than half of Indian households having a bank account in 2006, as my colleague Abhishek Waghmare found looking at National Family Health Survey data, to 96% of households having a bank account by 2021 is not just a big shift, it's a momentous shift. Moreover, since this is household survey data, we know that it's not just banks reporting that an account was created, but household heads actually reporting to surveyors that someone in the family now has a bank account.

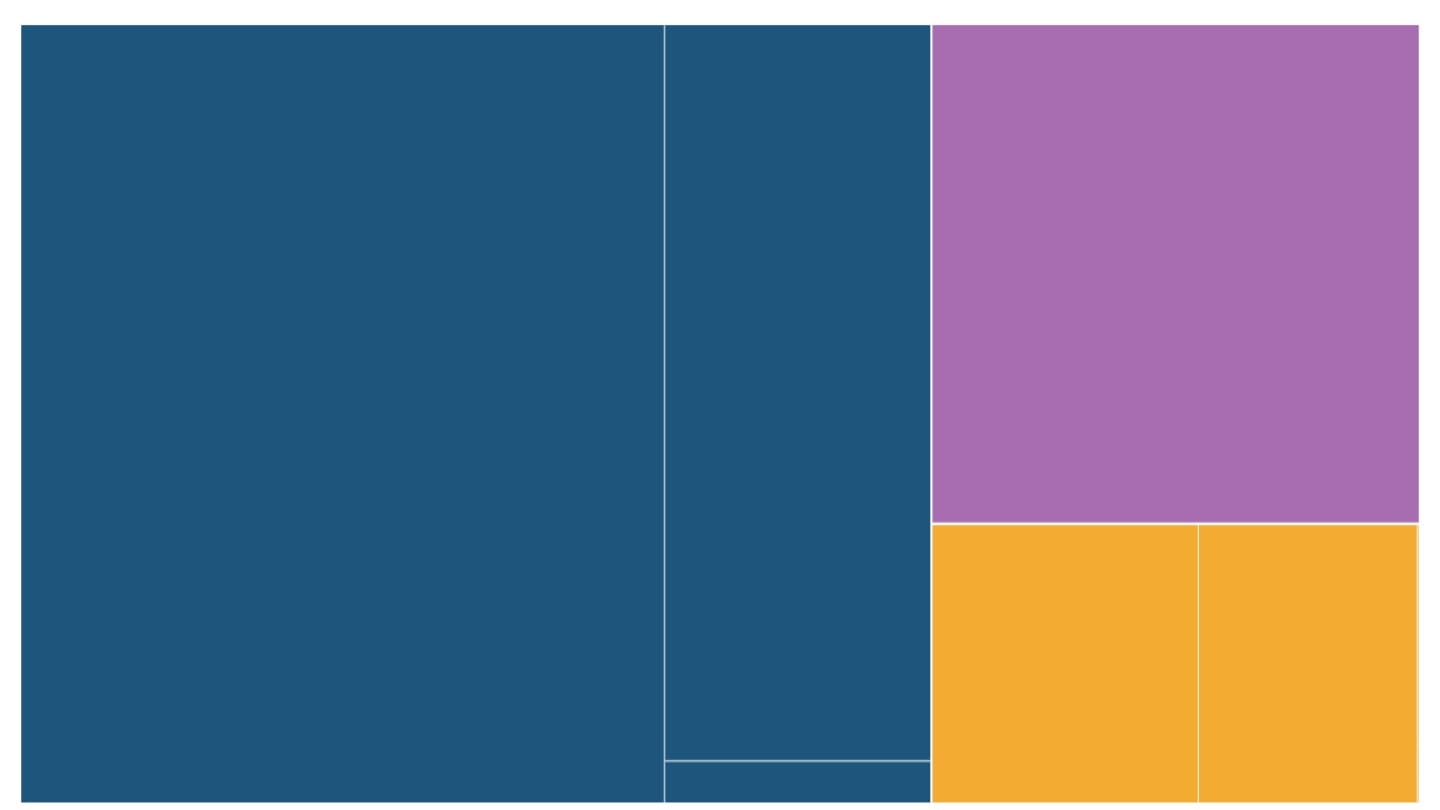

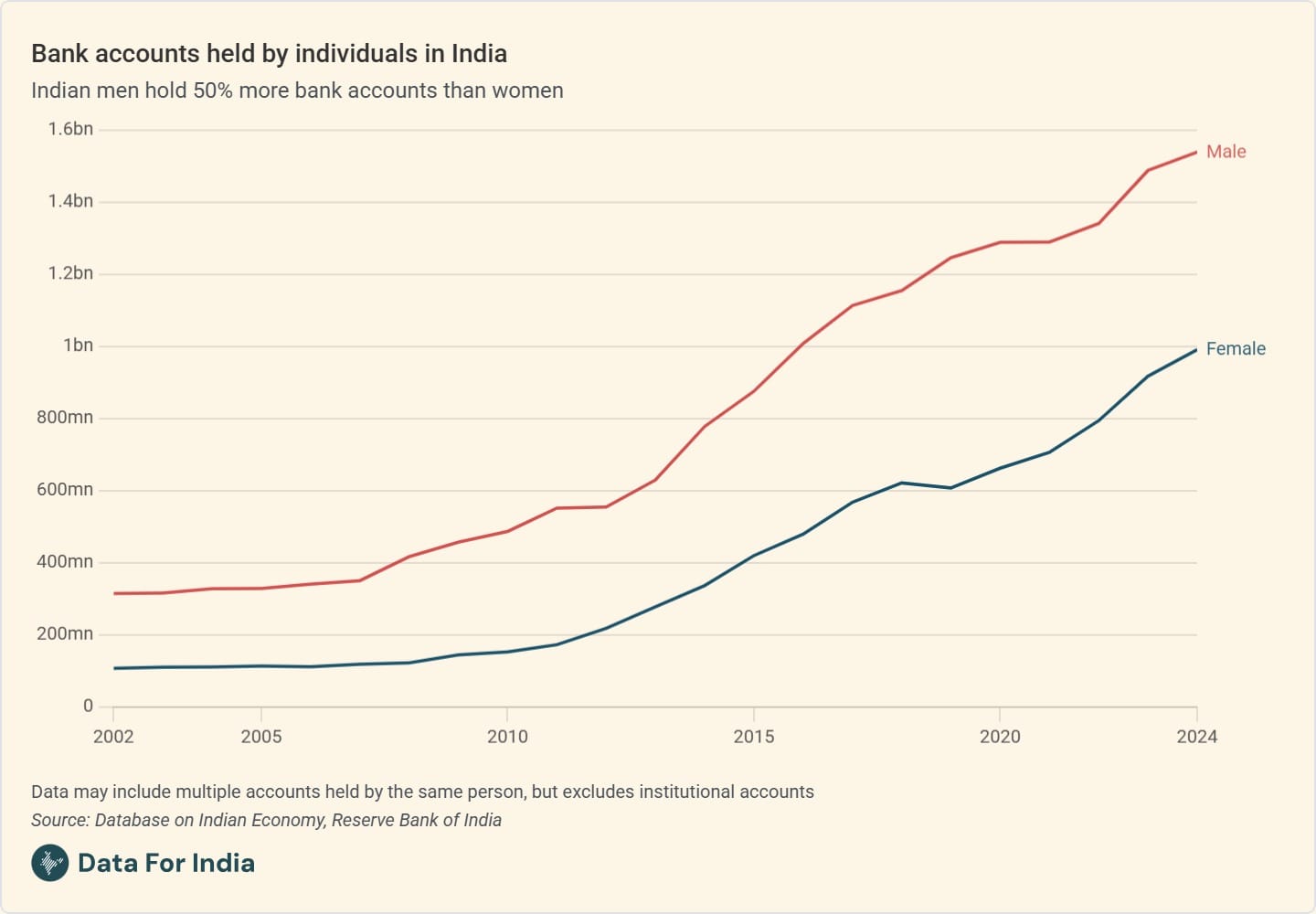

But within this, there were two data points that gave me some pause. First was this startling graph from Abhishek on the gender gap in individual bank account ownership.

You will notice immediately that the number of bank accounts is larger than the Indian population, and this is because some individuals may have more than one bank account. You will also notice that men in India have 50% more bank accounts than women. This gap is particularly large in some states, Abhishek finds.

The second data point that gave me some pause was not from our primary research, but came from Abhishek's reading of the World Bank's Global Findex Database that surveys representative samples in over 100 countries. The survey "found that more than a third of account-holders in India had an inactive account in 2021, meaning that they had made neither deposits nor withdrawals, nor had any incoming or outgoing digital payments in the preceding year," Abhishek writes. "Women were more likely to be holding inactive bank accounts. About 42% of female account owners in India were found to be having inactive accounts compared to 30% among male account owners. This gender gap was particularly large in India," he writes.

It seems very likely to me that these numbers may have shifted since 2021, given that big push to banking that the pandemic forced on us, so we will keep an eye out for when there's newer data. But one thing that we have learned is that even when trendlines grow, gaps - particularly those that break down around entrenched inequalities - take longer to shrink. Getting most Indians into the banking system has been one big shift, but making sure that everyone, especially women, is getting the full benefit of this inclusion will need its own push.