The extent of usage of phones and the internet by Indians is something that is usually talked of with such hyperbole, that it can be hard to spot a real big shift here any more. As we've looked at in our work on the usage of phones, the vast majority of Indians have a phone, but just one in four women have their own phones, for instance. Or, as I wrote in an earlier edition of this newsletter, the use of computers has not really taken off. But here's one area where the usage of mobile phone-based internet has not just seen a big shift, but a fair decimation of the rest of the field - retail payments.

Retail payments - transactions made to buy goods and services - can be made through cash and cheques, and a variety of digital methods including debit and credit cards, the National Electronic Fund Transfer (NEFT), the Immediate Payments Service (IMPS), and the Unified Payments Interface (UPI). (Here, we're looking at everything but cash which is harder to track, but my colleague Abhishek Waghmare has some telling numbers on the decline of cash in his piece for us.)

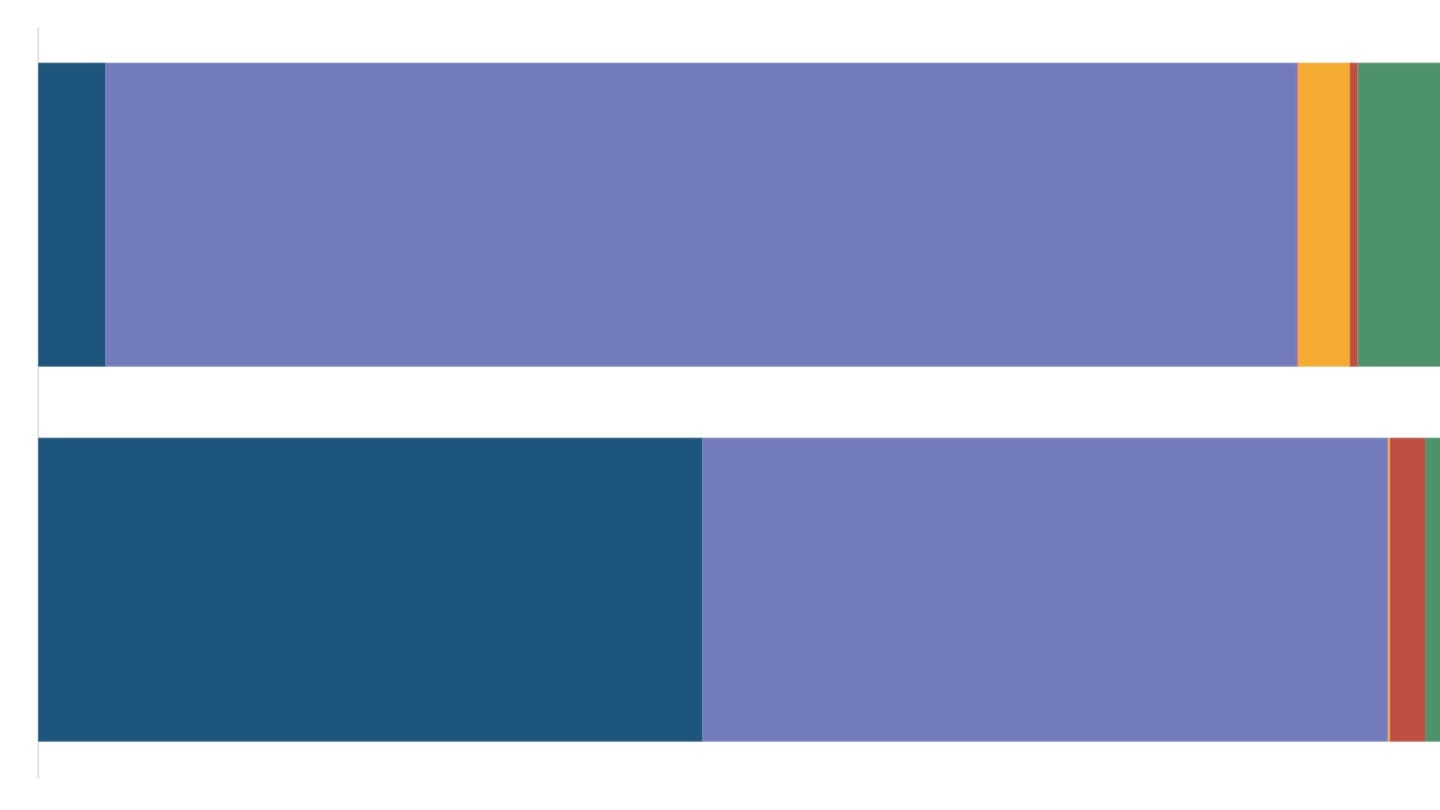

Digital retail payment modes have already eaten up paper payments. In 2005, 99% of the annual transacted value of retail payments was done through cheques. Twenty years later, Abhishek finds, cheques were down to just 8%, with NEFT now accounting for over half of the annual transacted value of retail payments, and UPI making up most of the rest.

But even among digital payment modes, we're seeing that this is now essentially a UPI game.

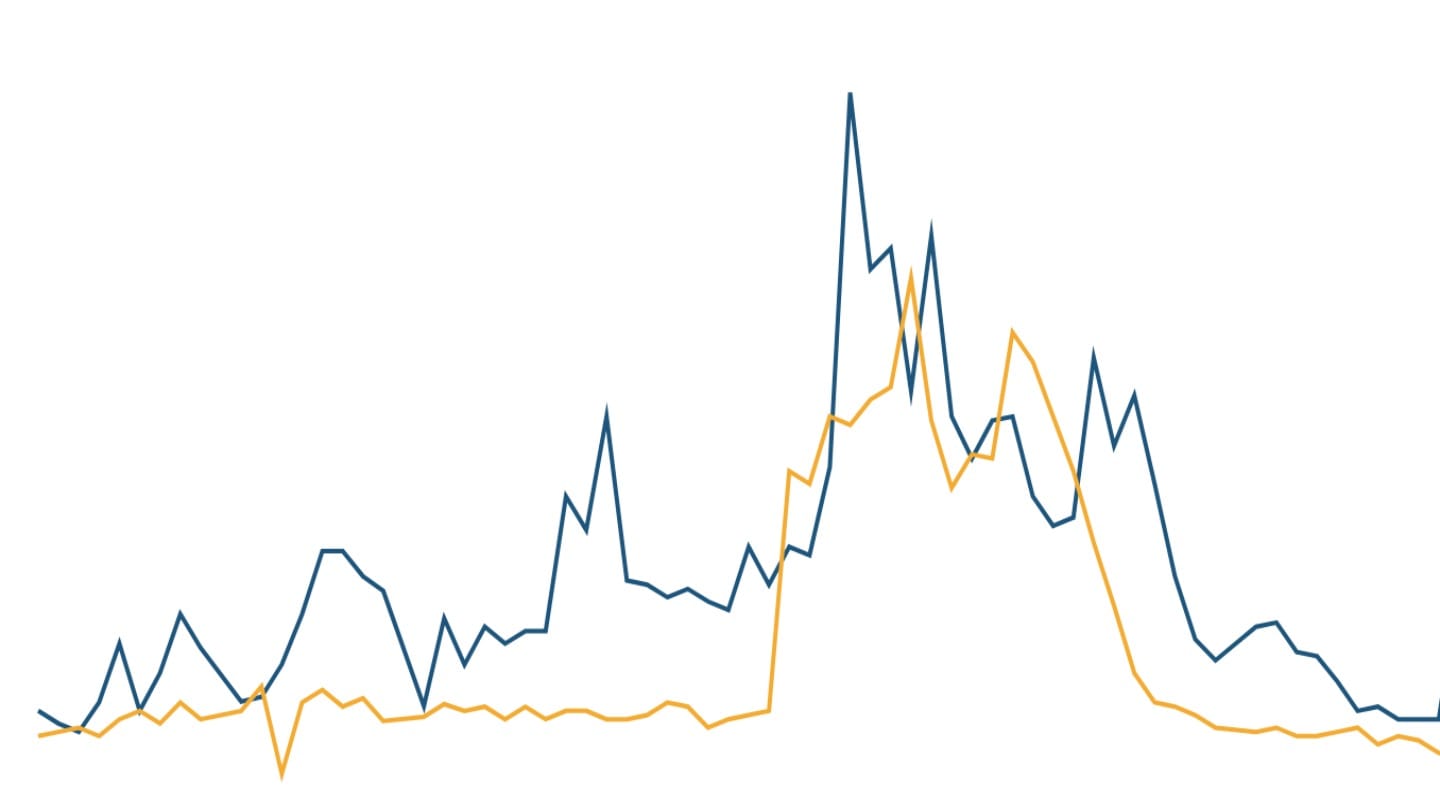

By 2019, the number of daily transactions made using UPI was a little over the number of daily transactions made using debit cards - roughly 40 million. In the five years since then, the increase in the usage of UPI has looked as much like a straight line as is possible. In the first month of 2025, there were 550 million transactions made every day using UPI. Debit card ownership, meanwhile, began plateauing from the late 2010s, Abhishek finds, and then the blow that the pandemic dealt their usage is something they've just not recovered from; to UPI's 550 million daily transactions, there were just four million daily transactions with debit cards in January 2025.

In terms of value, NEFT still accounts for the largest share - while the average value of a UPI transaction is around Rs 1,500, that of an NEFT transaction is a little under Rs 50,000. But here too, UPI is catching up.

One thing that you see with historical data is that every time a new mode of payment comes in (credit cards, debit cards, NEFT), you see a spike in their usage and older methods like cheques start to shrink in the chart. But the rise of UPI is unlike anything we've seen before in retail payments - it is unquestionably the biggest shift, and it continues to grow.